flowchart LR A[Product ontology] --> B[Treatment pathway] C[Indication context] --> B D[Funding and access] --> B B --> E[Persistence and switching] B --> F[Clinical outcomes] G[Behaviour and support] --> E G --> F D --> E

1 The Australian GLP-1 timeline

Australia’s GLP-1 market did not become important overnight. It moved through several phases: diabetes treatment, shortages, compounded alternatives, commercial obesity launches, and active PBS debate.

For Australian healthcare readers, GLP-1s are now an access, policy, supply, affordability, and real-world persistence problem. The same active molecule can sit in different brands, indications, doses, reimbursement pathways, and patient journeys. A dashboard that simply counts “GLP-1 scripts” can easily mix several different stories: subsidised type 2 diabetes treatment, private weight-management use, medicine switching during shortages, migration away from compounded replicas, clinical adoption after new evidence, and out-of-pocket discontinuation.

| Date | Public-market event | Why analysts should care |

|---|---|---|

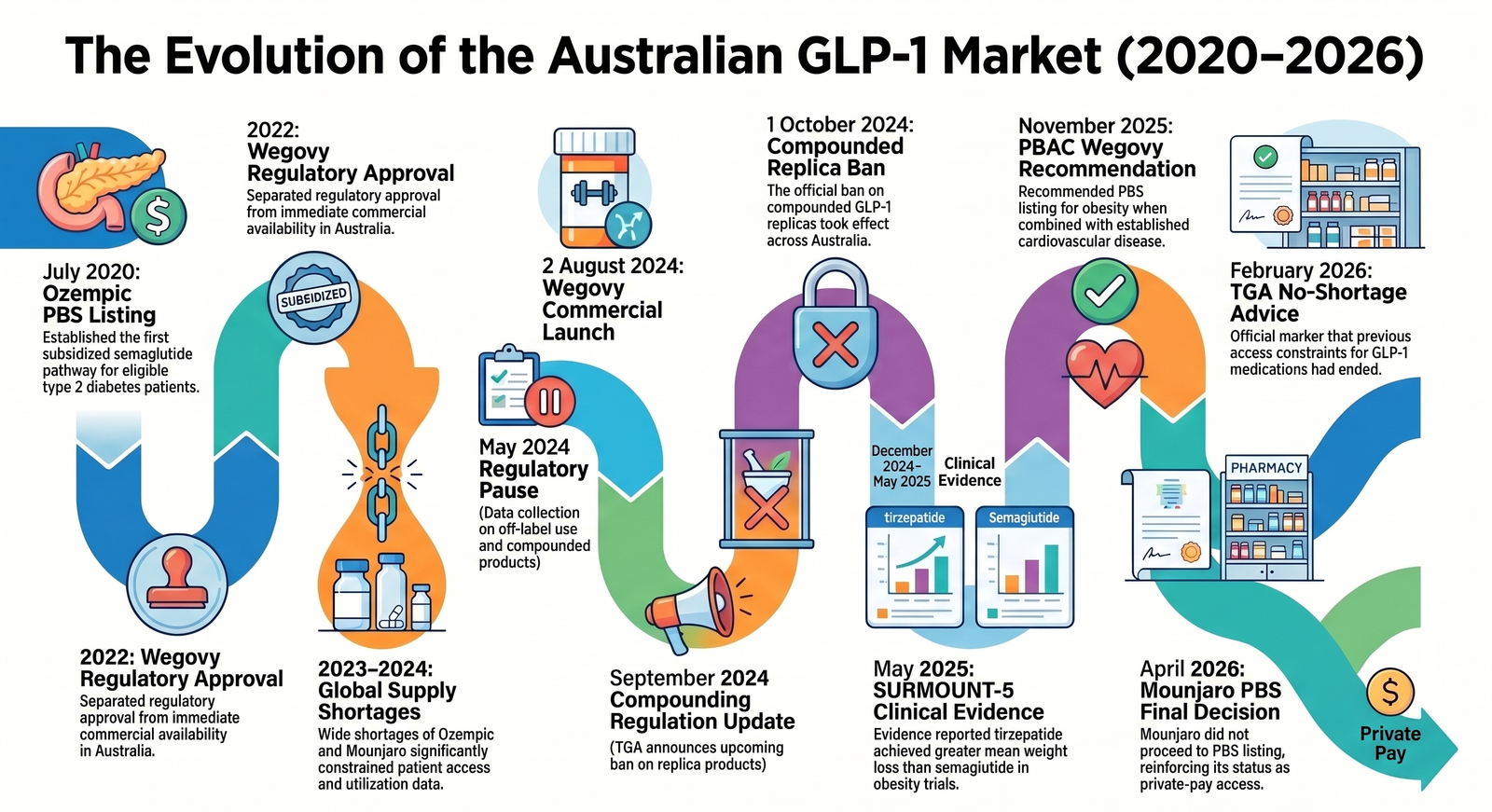

| July 2020 | Ozempic was listed on the PBS for eligible patients with insufficiently controlled type 2 diabetes. | Establishes the subsidised semaglutide diabetes pathway. |

| 2022 | Wegovy received Australian regulatory approval for chronic weight management, but was not immediately supplied locally. | Separates regulatory approval from commercial availability. |

| 2023-2024 | Ozempic and Mounjaro shortages were widely reported during a period of strong demand. | Utilisation data during this period can reflect supply constraint, not only patient demand. |

| May 2024 | The Australian Government announced changes to remove GLP-1 replica products such as compounded semaglutide and tirzepatide from pharmacy compounding exemptions. | Creates a major access and channel event for patients previously using compounded products. |

| 2 August 2024 | Wegovy was commercially launched in Australia. | Introduces a branded semaglutide product specifically positioned for weight management. |

| September 2024 | Mounjaro KwikPen availability expanded in Australia. | Improves practical access and usability for tirzepatide. |

| 1 October 2024 | The compounded GLP-1 replica ban took effect. | Important break point for market monitoring and demand interpretation. |

| December 2024-May 2025 | SURMOUNT-5 evidence reported greater mean weight loss with tirzepatide than semaglutide in a head-to-head obesity trial. | Supports stronger clinical and consumer attention around tirzepatide. |

| November 2025 | PBAC recommended Wegovy for PBS listing for people with established cardiovascular disease and obesity, subject to conditions. | Signals a potential pathway where obesity pharmacotherapy is framed through cardiovascular risk reduction. |

| February 2026 | PBS information stated that TGA advised there were no shortages of GLP-1 medication in Australia. | A useful marker that access constraints had changed versus the shortage period. |

| April 2026 | Eli Lilly Australia said Mounjaro would not proceed to PBS listing for type 2 diabetes under the proposed terms, after a positive PBAC recommendation. | Reinforces the private-pay nature of tirzepatide access at that point. |

The analytics lesson is simple: time matters. A GLP-1 trend line from 2023 to 2026 is not just a demand curve. It is overlaid with regulatory changes, supply disruption, new product availability, clinical evidence, and funding negotiations.

2 GLP-1 products and molecules currently available

“GLP-1” is often used as shorthand, but the analytics definition needs to be more precise.

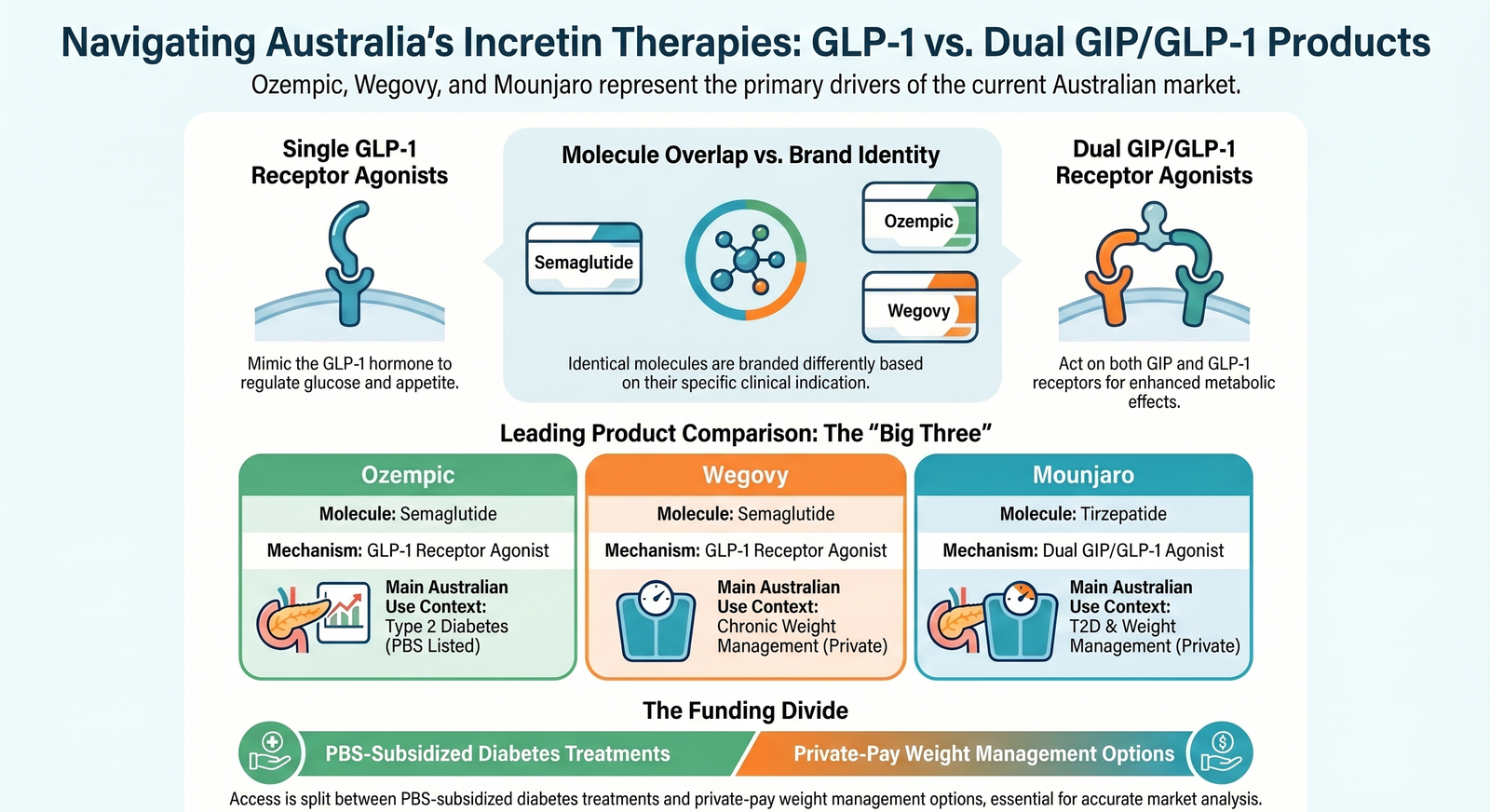

GLP-1 receptor agonists mimic or enhance the action of glucagon-like peptide-1, an incretin hormone involved in post-meal glucose control, insulin secretion, glucagon suppression, gastric emptying, appetite, and satiety. In practice, the Australian market includes both single GLP-1 receptor agonists and a dual GIP/GLP-1 agonist.

| Brand | Molecule | Mechanism | Main Australian use context |

|---|---|---|---|

| Ozempic | Semaglutide | GLP-1 receptor agonist | Type 2 diabetes; PBS listed for eligible patients |

| Wegovy | Semaglutide | GLP-1 receptor agonist | Chronic weight management; commercially available, with a narrow PBAC recommendation pathway for obesity plus established cardiovascular disease |

| Trulicity | Dulaglutide | GLP-1 receptor agonist | Type 2 diabetes; PBS listed |

| Saxenda | Liraglutide | GLP-1 receptor agonist | Chronic weight management |

| Victoza | Liraglutide | GLP-1 receptor agonist | Type 2 diabetes |

| Mounjaro | Tirzepatide | Dual GIP/GLP-1 receptor agonist | Type 2 diabetes and chronic weight management; private prescription as at May 2026 |

For data modelling, the key point is that brand, molecule, dose, indication, and reimbursement status should not be collapsed into one undifferentiated field. Ozempic and Wegovy both contain semaglutide, but they represent different approved use contexts and different access pathways. Mounjaro is even more distinct because tirzepatide acts on both GIP and GLP-1 receptors.

If a model groups all of these products together without flags for molecule, brand, indication, and funding status, it will be hard to interpret utilisation, persistence, switching, and affordability.

3 The access landscape as at May 2026

The Australian market can be understood through a simple access lens.

| Access pathway | Examples | Interpretation |

|---|---|---|

| PBS-subsidised diabetes treatment | Ozempic and Trulicity for eligible type 2 diabetes patients | Lower patient co-payment, clearer diabetes indication, stronger continuity if supply is stable |

| Private prescription for weight management | Wegovy, Saxenda, and private/off-label use depending on prescriber judgement and product indication | Higher out-of-pocket cost and more sensitivity to affordability |

| Private prescription for dual agonist therapy | Mounjaro as at May 2026 | Strong interest, but affordability and persistence are major issues |

| Potential future subsidised obesity/CVD pathway | Wegovy for established cardiovascular disease with obesity, following PBAC recommendation | A narrow but important policy signal; listing implementation depends on negotiation and final conditions |

| Former compounded replica pathway | Compounded semaglutide or tirzepatide replicas before 1 October 2024 changes | Relevant historically, but not an ongoing legal access pathway under the changed compounding exemption settings |

This is why “PBS versus private” is one of the most important variables in Australian GLP-1 analytics. It changes the population being observed.

A subsidised diabetes cohort and a private weight-management cohort may differ in diagnosis, age, comorbidity, prescriber type, affordability, refill behaviour, and discontinuation risk. Treating them as the same group can lead to weak conclusions.

4 Pricing and affordability are not side details

GLP-1 analytics is inseparable from affordability.

PBS-subsidised medicines are shaped by the standard PBS co-payment settings. Private GLP-1 use is different. Public reports and market commentary commonly describe private prices in the hundreds of dollars per month, with Mounjaro often described as materially more expensive than PBS-subsidised diabetes medicines.

For analysts, this affects three basic metrics:

- Initiation: who can start treatment when the monthly cost is high?

- Persistence: who can stay on therapy after three, six, or twelve months?

- Switching: does a patient switch molecule, dose, brand, or channel because of price, tolerability, supply, or clinical response?

In a private-pay market, discontinuation may not mean a medicine failed clinically. It may mean the patient could not afford to continue, could not access stock, experienced side effects, or moved to a different care model.

6 A practical Australian GLP-1 data model

For most healthcare analytics work, I would separate the data model into six layers.

| Layer | What to capture | Why it matters |

|---|---|---|

| Product ontology | Brand, molecule, mechanism, strength, dose form, pack, ARTG status | Prevents false grouping of semaglutide, liraglutide, dulaglutide, and tirzepatide |

| Indication context | Type 2 diabetes, chronic weight management, cardiovascular risk reduction, off-label inference where appropriate | Explains why the patient may be treated and which outcomes are relevant |

| Funding and access | PBS status, private status, co-payment, restriction criteria, supply constraints | Explains affordability and observed refill behaviour |

| Treatment pathway | Start, titration, dose escalation, interruption, restart, switch, stop | Separates adoption from sustained therapy |

| Clinical baseline and outcomes | BMI, HbA1c, cardiovascular disease, renal risk, weight, blood pressure, lipids, adverse events | Links utilisation to health outcomes |

| Behaviour and support | nutrition support, physical activity, side-effect management, follow-up cadence, digital support | Helps explain adherence and long-term maintenance |

This frame is broader than a medicine table because GLP-1 therapy behaves like a cross-system intervention. It touches general practice, endocrinology, obesity medicine, cardiology, pharmacy, dietetics, consumer health behaviour, and government reimbursement.

7 What healthcare AI must get right

GLP-1 is a useful test case for healthcare AI because the terminology is deceptively easy.

An AI system may see “Ozempic”, “Wegovy”, “semaglutide”, “Mounjaro”, “tirzepatide”, “weight loss injection”, and “diabetes medicine” and treat them as interchangeable. They are not interchangeable for analysis.

A reliable AI workflow needs to preserve context:

- brand versus molecule: Ozempic and Wegovy are both semaglutide, but not the same market object

- single versus dual agonist: tirzepatide is not simply another semaglutide brand

- indication: diabetes, obesity, and cardiovascular risk reduction are different analytic frames

- funding status: PBS and private-pay populations can behave very differently

- time period: a 2023 shortage-period record is not equivalent to a 2026 post-shortage record

- source type: TGA, PBS, PBAC, company releases, media reporting, and clinical trials have different evidentiary roles

The main AI risk is not that a model cannot summarise GLP-1 information. The risk is that it summarises confidently while losing the distinction that actually matters.

8 Key takeaways for Australian analysts

If you only remember five things, make them these:

- GLP-1 is not one market. It is diabetes care, obesity care, cardiovascular-risk policy, and private-pay access interacting at once.

- In Australia, PBS status is central. It determines who can afford treatment and how persistence should be interpreted.

- Semaglutide and tirzepatide should be modelled separately. Molecule and mechanism matter.

- The 2024 events matter: Wegovy’s commercial launch and the compounded replica ban are major timeline break points.

- Persistence is as important as initiation. A market can show strong starts while long-term continuation remains fragile.

9 Closing thought

GLP-1 analytics in Australia is moving from simple product tracking to a richer healthcare data problem.

The useful question is no longer only “how many scripts were supplied?” It is:

Which patients can access treatment, through which pathway, for which indication, at what cost, with what persistence, and with what outcome?

That is the knowledge foundation analysts need before building dashboards, forecasting models, cohort definitions, or AI summaries.

10 Sources

- Therapeutic Goods Administration. “Medicines containing GLP-1 and dual GIP/GLP-1 receptor agonists.” https://www.tga.gov.au/news/safety-updates/medicines-containing-glp-1-and-dual-gipglp-1-receptor-agonists

- Therapeutic Goods Administration. “Product warnings updated for GLP-1 RA class.” https://www.tga.gov.au/safety/safety-monitoring-and-information/safety-alerts/product-warnings-updated-glp-1-ra-class

- Pharmaceutical Benefits Scheme. “PBAC advice on equitable access to GLP-1 obesity treatments.” https://www.pbs.gov.au/info/reviews/PBAC-advice-equitable-access-to-GLP-1-obesity-treatments

- Diabetes Australia. “Wegovy to be listed on PBS.” https://www.diabetesaustralia.com.au/news/wegovy-to-be-listed-on-pbs/

- Health.gov.au. “Protecting Australians from unsafe compounding of replica weight loss products.” https://www.health.gov.au/ministers/the-hon-mark-butler-mp/media/protecting-australians-from-unsafe-compounding-of-replica-weight-loss-products

- Eli Lilly Australia. “No PBS listing for Mounjaro (tirzepatide) in type 2 diabetes.” https://newshub.medianet.com.au/2026/04/no-pbs-listing-for-mounjaro-tirzepatide-in-type-2-diabetes/149901/

- Eli Lilly and Company. “Zepbound (tirzepatide) showed superior weight loss over Wegovy (semaglutide) in complete SURMOUNT-5 results.” https://investor.lilly.com/news-releases/news-release-details/zepboundr-tirzepatide-showed-superior-weight-loss-over-wegovyr

- Prime Therapeutics. “Real-world GLP-1 obesity treatment adherence and persistency year two study.” https://www.primetherapeutics.com/news/real-world-glp-1-obesity-treatment-adherence-and-persistency-year-two-study/

- Blue Cross Blue Shield Health Institute. “Real-world trends in GLP-1 treatment persistence and prescribing for weight management.” https://www.bcbs.com/the-health-of-america/reports/real-world-trends-glp-1-treatment-persistence-and-prescribing-weight-management